Research: Global cloud infrastructure spend up 25% in Q3

December 22, 2025

According to research from Omdia, global spending on cloud infrastructure services reached $102.6 billion (€87.3bn) in Q3 2025, representing 25 per cent year-on-year growth. Market momentum remained stable, marking the fifth consecutive quarter in which growth has remained above 20 per cent highlighting continued strength across the sector. This performance reflects a significant shift in the technology landscape as enterprise demand for AI moves beyond early experimentation toward scaled production deployment. As this transition accelerates, hyperscalers are increasingly redirecting competition away from the incremental gains in model performance and toward platform-level capabilities that support multi-model deployment and ensure the reliable operation of AI agents in real-world environments.

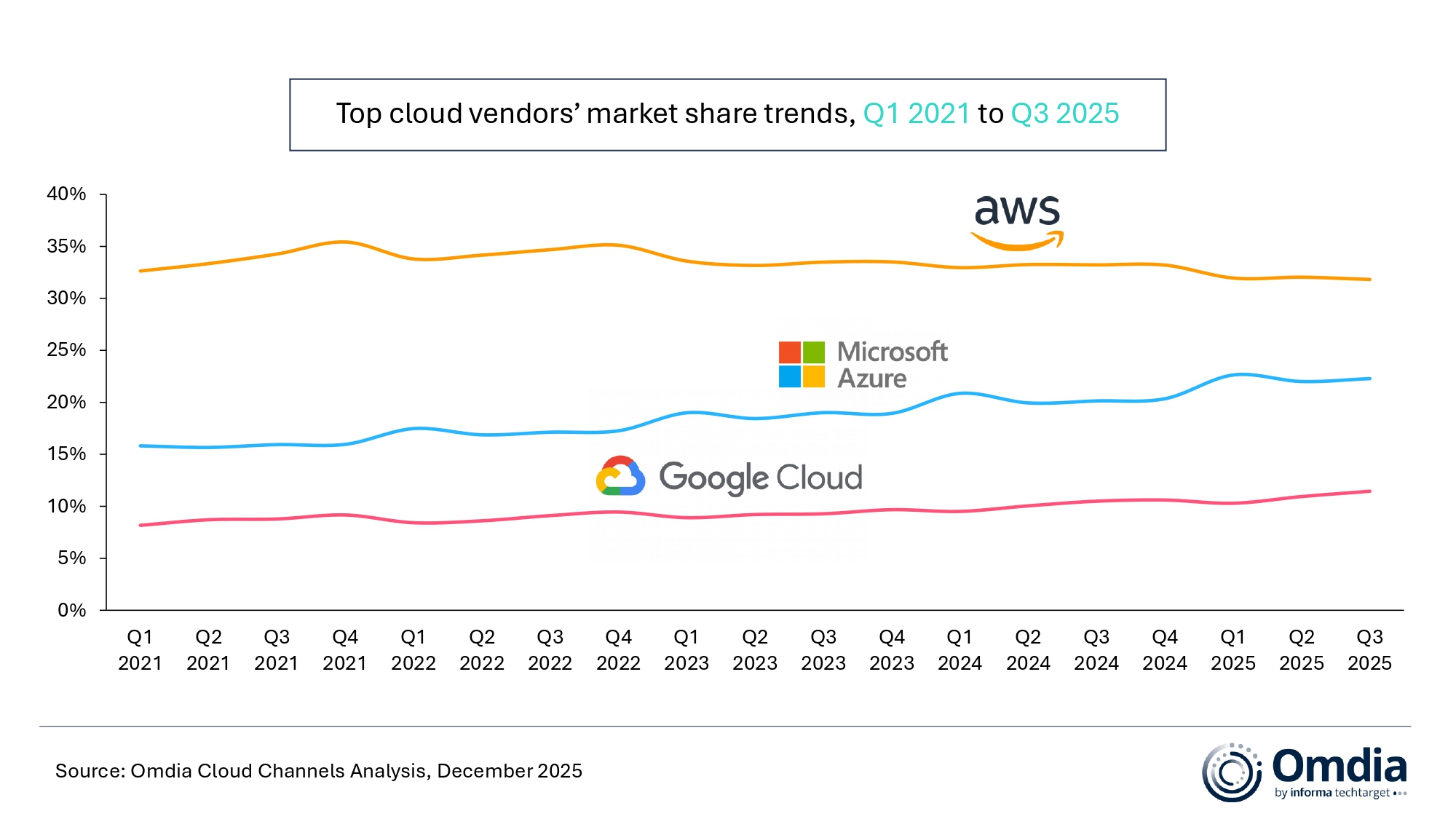

In Q3 2025, AWS, Microsoft Azure, and Google Cloud maintained their market rankings from the previous quarter, collectively accounting for 66 per cent of global cloud infrastructure spending. Together, the three hyperscalers delivered 29 per cent year-on-year growth.

AWS’s growth reaccelerated to 20 per cent year on year quartering Q3 2025, marking its strongest performance since 2022. Microsoft Azure and Google Cloud also maintained strong momentum, each delivering year-on-year growth of more than 35 per cent. As enterprise demand for AI continues to materialise, growth in the cloud market is shifting from early-stage experimentation and pilot projects toward the scaled deployment of enterprise-grade AI applications. Backlog levels among leading cloud providers continued to rise, with AWS, Microsoft and Google Cloud all reporting further increases in Q3 order backlogs, reinforcing the market’s underlying resilience and healthy demand environment.

Hyperscalers’ AI strategies are evolving from a primary focus on incremental model performance toward more platform-driven and production-ready approaches. Enterprises are no longer evaluating AI platforms solely on model capabilities, but increasingly on their support for multi-model strategies and agent-based applications.

This shift is accelerating hyperscalers’ move toward platform-level AI capabilities. AWS, Microsoft Azure, and Google Cloud are integrating proprietary foundation models with a growing range of third-party and open-weight models, leveraging managed AI platforms and services such as Amazon Bedrock, Azure AI Foundry, and Vertex AI’s Model Garden to expand support for multi-model adoption.

“Collaboration across the ecosystem remains critical,” said Rachel Brindley, Senior Director at Omdia. “Multi-model support is increasingly viewed as a production requirement rather than a feature, as enterprises seek resilience, cost control, and deployment flexibility across generative AI workloads.”

Meanwhile, hyperscalers are stepping up investment in agent build-and-run capabilities, as real-world deployment continues to prove more complex than early experimentation suggested. “Many enterprises still lack standardised building blocks that can support business continuity, customer experience, and compliance at the same time, which is slowing the real-world deployment of AI agents,” said Yi Zhang, Senior Analyst at Omdia. “This is where hyperscalers are increasingly stepping in, using platform-led approaches to make it easier for enterprises to build and run agents in production environments.”

Recent launches such as AWS AgentCore and Microsoft’s Agent Framework reflect this direction, providing standardised foundational capabilities that help enterprises more efficiently build, deploy, and operate AI agents in production settings.

Amazon Web Services (AWS) led the global cloud infrastructure market with a 32 per cent share and 20 per cent year-on-year revenue growth. This performance was supported by easing compute supply constraints, alongside incremental demand driven by its partnership with Anthropic. AWS reported a total backlog of $200 billion by the end of Q3, underscoring sustained demand. Amazon Bedrock continues to evolve rapidly, expanding both model choice and platform capabilities, including support for Claude 4.5, 18 managed open-weight models, and enhanced Guardrails and Data Automation features. At AWS re:Invent 2025, AWS also introduced the Nova 2 model family, Nova Act, and Nova Forge, strengthening its end-to-end enterprise AI stack from models to agents and automation. In addition, AWS expanded its regional footprint with the launch of the AWS Asia Pacific (New Zealand) Region in September, adding three availability zones to support local data residency and low-latency workloads.

Microsoft Azure remained the world’s second-largest cloud provider in Q3 2025, holding a 22 per cent market share and delivering robust 40 per cent year-on-year revenue growth. In October, Microsoft renewed its partnership with OpenAI, further anchoring OpenAI’s AI development and deployment on Azure. Azure AI Foundry continued to broaden its model ecosystem, supporting multiple frontier foundation models, including Claude Opus 4.5, Claude Sonnet 4.5, and Haiku 4.5. The platform now serves more than 80,000 customers and provides access to over 11,000 models. In October, Microsoft also introduced the Microsoft Agent Framework, enabling enterprises to build and orchestrate multi-agent systems. Customers such as KPMG are already applying the framework to enhance audit processes, with these production-grade AI deployments contributing to Azure’s overall growth momentum. In parallel, Microsoft continued to invest in regional infrastructure, announcing plans in November to expand its Azure cloud region in Malaysia and to launch a new Azure datacenter region in India in 2026.

Google Cloud remained the world’s third-largest cloud services provider in Q3 2025, delivering strong 36 per cent year-on-year growth and increasing its market share to 11%. Growth was primarily driven by enterprise AI offerings, with quarterly revenue from this segment reaching several billion dollars. As of September 30, Google Cloud reported a backlog of $157.7 billion, up sharply from $108.2 billion in Q2, underscoring strengthening demand visibility. On the platform side, Vertex AI’s Model Garden continued to expand its large-scale AI model portfolio, adding new models such as multimodal variants from the Gemini 2.5 series, Kimi K2 Thinking, and DeepSeek-V3.2. In October 2025, Google Cloud also launched Gemini Enterprise, an AI platform designed for enterprise customers that integrates the Gemini model family with enterprise-grade AI agents, no-code development tools, and security and governance capabilities.

(Omdia defines cloud infrastructure services as the sum of bare metal as a service (BMaaS), infrastructure-as-a-service (IaaS), platform-as-a-service (PaaS) and container-as-a-service (CaaS) and serverless that are hosted by third-party providers and made available to users via the Internet.)

Other posts by :

- Bank: Opportunities for SES and Eutelsat

- Bank: SES outperforming

- AST SpaceMobile confirms 2026 launch schedule

- AST SpaceMobile: “Good for indoor reception”

- EchoStar booms on SpaceX holding

- Norway wants a satellite constellation

- Crossroads backs AST SpaceMobile

- FCC examines SpaceX’s 15,000 sat-constellation plan

- EchoStar: “Severe uncertainty” led to spectrum sales